Cabarrus County FY 2027 Adopted Budget

Debt Service

County debt service, legal debt margin, and related schedules.

Debt Service Overview

Debt Service

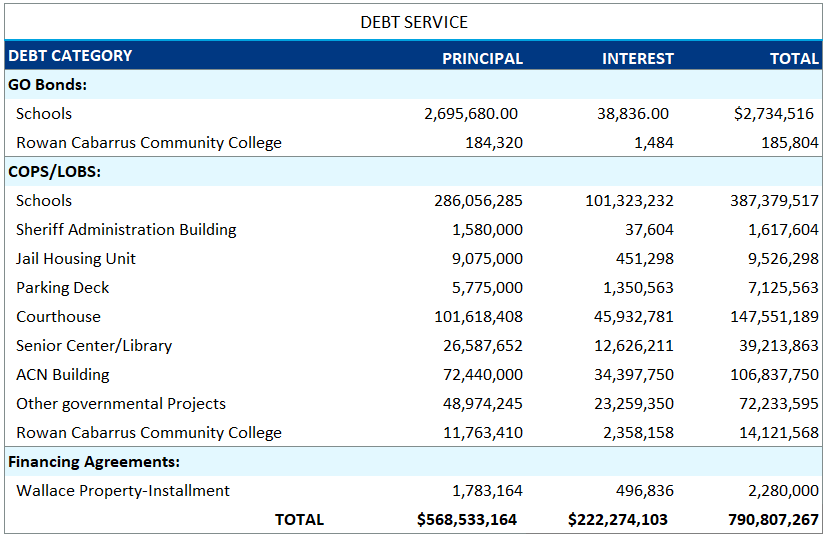

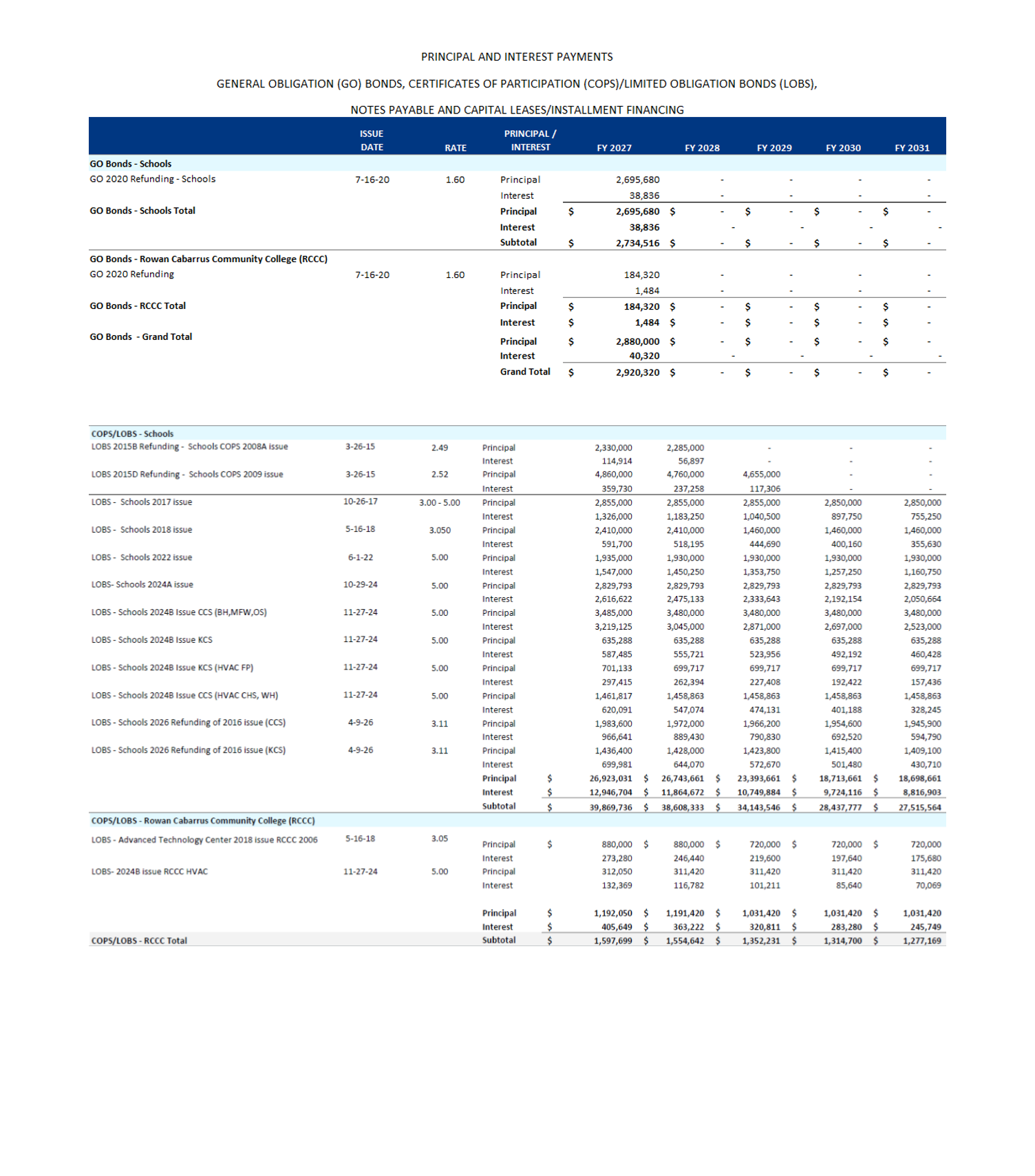

is mandated by G.S. 159-36, 159-25(a) (5). The Community Investment Fund (CIF) is maintained to track the annual principal and interest requirements of General Obligation Bonds (GO), Certificates of Participation (COPS)/Limited Obligation Bonds (LOBS) and Lease and Installment Financing Agreements. The County has the following principal and interest debt outstanding as of June 30, 2026:

Note

The COPS 2011A (Qualified School Construction Bonds) issue requires that annual principal payments be made to a sinking fund, held by a trustee, in the County's name. Annual budgeted payments of $1,330,000 are required for fiscal years 2016-2025 and a budgeted payment of $1,335,000 is required in fiscal year 2026. The trustee will make debt service payments of $7,200,000 and $7,435,000 from the sinking fund in fiscal years 2023 and 2026, respectively. At this time, the County will will record debt service expenditures and reduce its long-term liabilities. The accumulation of annual sinking fund payments will be accounted for in restricted fund balance. Therefore, the County will appropriate restricted fund balance in fiscal years 2023 and 2026 to fund the debt service expenditures.

Legal Debt Margin

June 30, 2026 North Carolina General Statute 159-55 limits the County's outstanding debt to 8% of the appraised value of property subject to taxation. The following deductions are made from gross debt to arrive at net debt applicable to the limit: money held for payment of principal; debt incurred for water, sewer, gas, or electric power purposes; uncollected special assessments, funding and refunding bonds not yet issued; and revenue bonds. The legal debt margin is the difference between the debt limit and the County's net debt outstanding applicable to the limit and represents the County's legal borrowing authority.