Cabarrus County FY 2027 Adopted Budget

Financial Structure

Fund structure and relationships, accounting basis, budgetary policies, and the budget process and calendar.

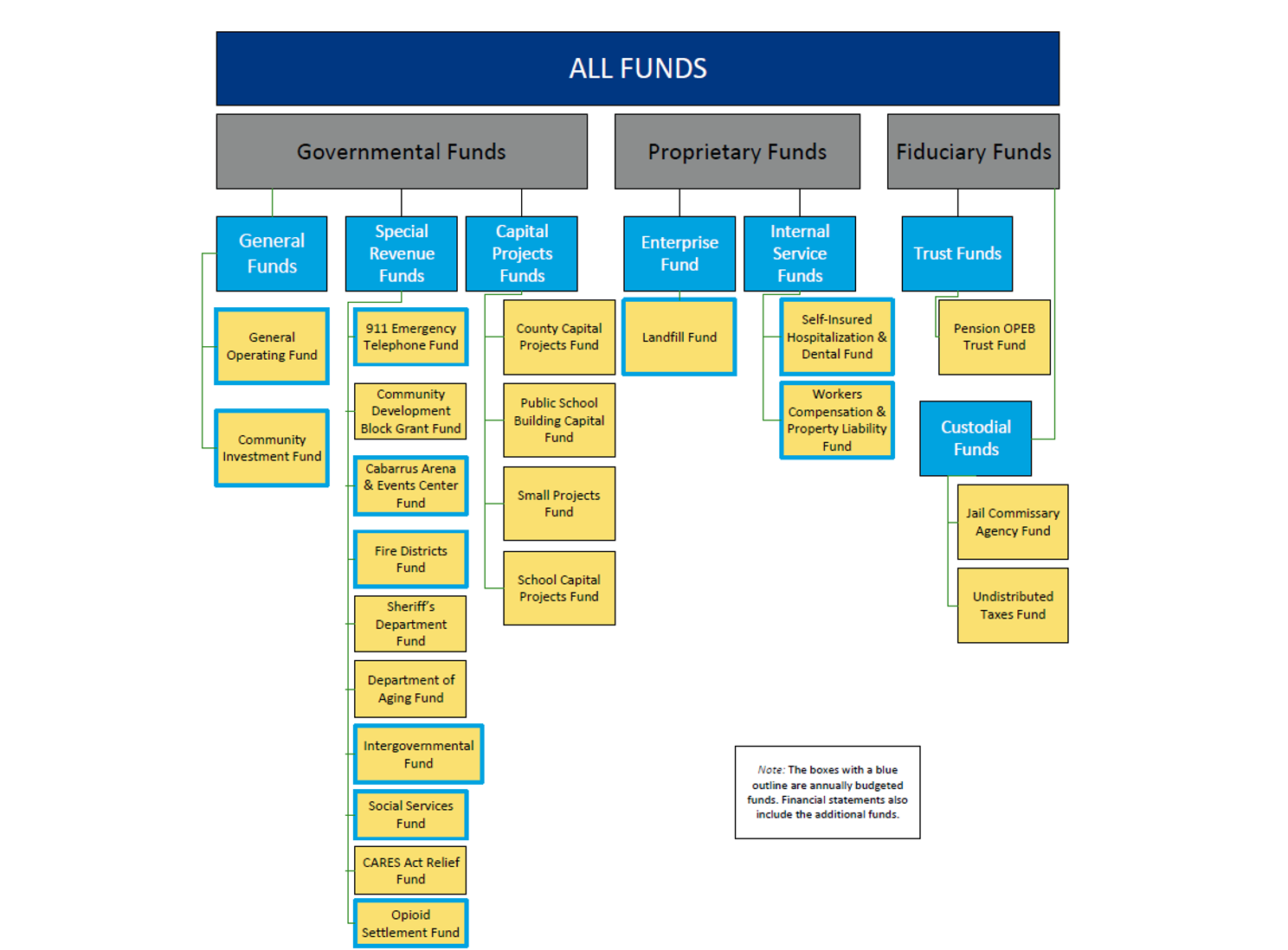

Fund Structure

Fund Relationships

Cabarrus County organizes and operates accounts by fund. A fund is an independent set of accounts where the county records financial transactions. The county maintains the minimum number of funds required by law. In addition, the County maintains additional sub-funds for specific management needs. The County has the following funds and sub-funds:

GENERAL FUNDS

- 001 - General Operating Fund

- 100 - Community Investment Fund

SPECIAL REVENUE FUNDS

- 401 - 911 Emergency Telephone System Fund

- 410 - Community Development Block Grant Fund

- 420 - Cabarrus Arena & Events Center Fund

- 430 - Fire Districts Fund

- 440 - CARES Relief Fund

- 442 - Opioid Settlement Fund

- 461 - Sheriff's Department Fund

- 532 - Department of Aging Fund

- 560 - Social Services Fund

- 571 - Intergovernmental Fund

CAPITAL PROJECTS FUNDS

- 320 - Public School Capital Fund

- 340 - County Capital Projects Fund

- 390 - School Capital Projects Fund

- 460 - Small Projects Fund

ENTERPRISE FUND

- 270 - Landfill Fund

INTERNAL SERVICE FUNDS

- 600 - Workers Compensation & Property Liability Fund

- 610 - Self-Insured Hospitalization & Dental Fund

TRUST FUNDS

- 550 - Pension OPEB Trust Fund

CUSTODIAL FUNDS

- 540 - Jail Commissary Agency Fund

- 570 - Undistributed Taxes Fund

General Operating Fund -

This fund is the primary operating fund for the County. Community Investment Fund - Sub-fund to account for sales tax/lottery revenue dedicated to school capital and property tax revenues for debt/capital projects. This sub-fund accounts for debt service expenditures and transfers to Capital Projects Funds.

SPECIAL REVENUE FUNDS - These funds account for revenues legally restricted to specific expenditures.

911 Emergency Telephone System Fund - Sub-fund to account for revenues received from subscriber fees specifically restricted for the operation and maintenance of a countywide Emergency 911 network. Community Development Block Grant (CDBG) Fund - Sub-fund to account for revenues received under the Community Development Block Grant Program specifically restricted to the revitalization of select areas of the County. Cabarrus Arena and Events Center Fund - Sub-fund to account for revenues received from rental, user fees and fund balance support specifically restricted to the operation of the facility. Fire Districts Fund - Sub-fund to account for property taxes collected and disbursed on behalf of the Fire Departments that protect the unincorporated areas of the County. Sheriff's Department Fund - Sub-fund to account for the collection and appropriation of federal and state funds received for the Cabarrus County Sheriff's Office. Department of Aging Fund - Sub-fund to account for the activities associated with contributions for senior citizen activities and projects. Social Services Fund - Sub-fund to account for moneys held by the Department of Human Services as agent for various individuals who are incapable of managing their own financial affairs. Intergovernmental Fund - Sub-fund to account for the accumulation of fines and forfeitures before they are distributed to the local School Boards. CARES Act Relief Fund- Sub-fund accounts for funding received from the federal government to cover COVID-19 expenditures for public health emergency. Opioid Settlement Fund - Sub-fund account for funding received from settlement proceeds from the national settlement agreement of the state and national litigation related to the opioid industry, including the manufacturing, marketing, promotion, distribution, and dispensing of opioids.

CAPITAL PROJECTS FUNDS - These funds account for the financial resources used for the acquisition or construction of major capital facilities other than those financed by proprietary and trust funds.

County Capital Projects Fund - constructs, renovates, and equips capital projects for the County through the use of debt and non-debt sources. Public School Building Capital Fund - Sub-fund collects state public school funds and lottery proceeds and disbursing the funds for smaller non-debt school capital projects. Small Projects Fund - Sub-fund collects and appropriates general fund revenues and federal and state grant funds received specifically for use by the appropriate Cabarrus County Department who has received the funds. School Capital Projects Fund - This sub-fund accounts for planning, design, construction and/or renovation of schools using debt and non-debt sources.

PROPRIETARY FUNDS

Enterprise Fund -

This fund accounts for operations financed and operated in a manner similar to private business enterprise. The intent of the county is to recover the cost of the service(s) through fees charged to users. Landfill Fund - Sub-fund to account for the operations of the solid waste landfill. Cabarrus County accepts demolition and recycled materials at the landfill. Most funds reserved in this fund are for post-closure expenditures related to future closure of the landfill. Internal Service Fund - This fund accounts for the financing of goods or services provided by one department or agency to another or to other government units on a cost reimbursement basis. Self-Insured Hospitalization and Dental Fund - Sub-fund to account for the administration and operation of the County's healthcare and dental insurance. Workers Compensation and Property Liability Fund - Sub-fund to account for the administration and operation of the County's self-funded workers compensation and property liability transactions.

FIDUCIARY FUNDS

Custodial Fund -

This fund is used to report assets held in a trustee or agency capacity for others and, therefore, cannot be used to support the government's own programs. The fiduciary fund category includes pension (and other employee benefit) trust funds, private-purpose trust funds and agency funds. Jail Commissary Fund - Sub-fund to account for the collection and disbursement of jail inmate's personal money. Undistributed Taxes Fund - Sub-fund to account for the collection of property taxes and the disbursement of the taxes to the county and to the municipalities located in the county.

TRUST FUNDS

Pension OPEB Trust Fund - Sub-fund to account for health care benefits of a single employer defined benefit Health Care Plan which provides postemployment health care benefits to eligible retirees of the county who participate in North Carolina Local Government Employees' Retirement System.

In accordance with North Carolina General Statues, all funds (governmental, proprietary and fiduciary) of the County are budgeted and accounted for on a modified accrual basis. Under this basis,

- The county recognizes Revenues in the accounting period they become measurable and available. Property tax revenue recognized in the fiscal year when taxes levied. Grant, entitlement and donation revenue recognized in the fiscal year when eligibility requirements were satisfied.

- The county recognizes Expenditures in the period incurred. One exception is principal and interest on general long-term debt, claims and judgments and compensated absences, which are expenditures in the year payments are due.

- The county financial statements for governmental funds use the current financial resources measurement focus.

- The county financial statements for proprietary and fiduciary funds use the economic resources measurement focus and the accrual basis of accounting, except for the Agency Funds which have no measurement focus.

The county uses formal budgetary accounting as a management control for all funds. Each fiscal year, the Board of Commissioners adopts an annual budget ordinance. In addition, the Board of Commissioners adopts project budgets that cover more than one fiscal year for specific revenue and capital project funds. Examples include the Community Development Block Grant (CDBG) and school construction. Each department exercises budgetary control, at the line item level, with the adoption of the budget by the Board of Commissioners. The county's fiscal year covers July 1 through June 30 of the budget year. Throughout the year, the Finance Department and the County Manager's office monitor expenditures and revenues. The Board of Commissioners, County Manager and Budget Director have authority to amend the budget during the fiscal year consistent with the adopted budget ordinance. The County Manager's Office and Finance Department ensure compliance with all purchasing and payment policies and procedures. The Finance Department also pre-audits all transactions to ensure compliance with the law.

- To maintain the County's stable financial position.

- To ensure implementation of adopted policies in an efficient and effective manner.

- To secure the highest possible credit and bond ratings by meeting or exceeding the requirements of bond rating agencies through sound, conservative financial decision making.

- To comply with all legal requirements.

Operating Budget Summary

The County's Annual Budget Ordinance is balanced in accordance with the Local Government Budget and Fiscal Control Act (N.C.G.S. 159-8 (a)). A balanced budget means that revenues or appropriated fund balance is equal to expenditures. The County's Annual Budget Ordinance is adopted by July 1 (N.C.G.S. 159-13 (a)). The County reviews financial policies annually in the following areas: Revenue Policy The County seeks to have diverse revenues to provide stability for consistent service levels and to protect against economic downturns. Revenue management is an ongoing process for reviewing and analyzing revenues to ensure proceeds are at an optimum level. The county estimates revenues conservatively based on trends and the economy. To meet these objectives the County observes the following guidelines: Ad Valorem (Property) Tax As provided by the North Carolina Local Budget and Fiscal Control Act, estimated revenue from the Ad Valorem Tax levy is budgeted as follows:

The county estimates assessed valuation conservatively based on historical trends and growth patterns. In accordance with state law, the estimated tax collection rate will not exceed the rate from the preceding fiscal year. The tax rate will be set each year based on the cost of providing general governmental services and paying debt service.

User Fees When the county can individually identify a service and its costs, the County maximizes user fees rather than property taxes. This objective is in keeping with the Commissioners' goal that growth should pay for itself and not place a burden on residents who do not use the service. Emphasis on user fees over property taxes results in the following benefits:

All users, even those that do not pay property taxes, pay user fees. User fees prevent the county from subsidizing services not provided to the public. User fees are a means to ration the provision of certain services. User fees are equitable and efficient. User fees connect an amount paid to a service received.

Grant Funding

The county will pursue opportunities for grant funding when aligned to Board of Commissioner priorities.

Other Revenue

The county appropriates all other revenue through the annual budget process to meet County Commissioner priorities.

Expenditure Policy

The county proactively monitors expenditures to maintain compliance with all requirements. Staff monitor expenditures throughout the year to ensure expenditures do not exceed revenues. The annual budget ordinance defines staff authorized to make budget adjustments during the fiscal year.

The county may only use debt proceeds for the issued purpose or payment of debt principal and interest. Similarly, the county can only spend donations for the stated purpose. For continuing contracts, the county appropriates funds in the annual budget ordinance to meet current year obligations, in accordance with G.S. 160A-17. Payroll is in accordance with the requirements of the Fair Labor Standards Act. Overtime and benefit payments are made in accordance with the County's Personnel Ordinance.

Fund Balance Policy

The County will maintain sufficient fund balance to address unanticipated revenue declines, avoid short-term borrowing and cover unbudgeted expenditures resulting from emergencies, natural disasters or unexpected opportunities. The County will not appropriate fund balance for ongoing operating expenditures except in extreme emergencies. Notwithstanding any other provisions of this policy, the County may appropriate fund balance for any use in the general fund to overcome revenue shortfalls related to significant downturns in the economy. The Local Government Commission (LGC) requires the county to maintain a minimum unassigned fund balance of 8% of general fund expenditures; however, it is the policy of the County to maintain unassigned fund balance equal to 15% of general fund expenditures.

A replenishment period commences if unassigned fund balance falls below 15%. Funds will be budgeted beginning with the subsequent fiscal year's adopted budget with a replenishment period not to exceed three consecutive fiscal years.

Following the completion of the annual financial audit, any unassigned fund balance above 15% transfers to the Community Investment Fund (CIF) or Capital Reserve Fund to reduce reliance on debt; and/or to the Self-Funded Hospitalization and Dental Fund, Workers Compensation and/or Liability Fund to maintain fund integrity.

Community Investment Fund Policy

The County maintains the Community Investment Fund (CIF) within the general fund to account separately for capital projects and debt. As a means to manage fund balance during both strong economic conditions and downturns, the county will maintain a minimum fund balance within the CIF of 25-35 percent. A replenishment period will commence if CIF fund balance falls below 25 percent. Funds will be budgeted beginning with the subsequent fiscal year's adopted budget with a replenishment period not to exceed three consecutive fiscal years.

Funding within the CIF will go toward the county's five-year capital improvement plan (CIP) which projects capital needs and expenditures and details the estimated cost, description and anticipated funding sources for capital projects. The first year of the CIP will be the basis of formal appropriations during the annual budget process. If new project needs arise during the year, a budget amendment will identify the funding sources and project appropriations to provide formal budgetary authority for the project. The CIP generally addresses capital projects with a value of more than $100,000 and a useful life of over five (5) years.

The County will emphasize preventive maintenance as a cost-effective approach to infrastructure maintenance. The County maximizes the use of pay-as-you-go (PAYGO) funding for capital projects to reduce the need for debt financing.

Debt Management Debt for capital projects will not exceed the expected useful life of the project.

The County will maximize the use of pay-as-you-go (PAYGO) funding for capital projects to reduce the need for debt. The general obligation debt of the County will not exceed eight percent of the assessed valuation of taxable property. General fund debt service will not exceed limits imposed and recommended by the Local Government Commission (LGC). The county closely monitors the formulas established by the LGC and rating agencies to make sure they are appropriately applied.

The County seeks the best financing type based on the following considerations: flexibility to meet the project needs, timing, payer equity and lowest interest cost.

The County strives for the highest possible bond rating to minimize the County's interest expenditures.

The County's debt policy is comprehensive and the County will not knowingly enter into any contracts creating significant unfunded liabilities.

Accounting/Financial Reporting Policy

The County will maintain an accounting system to monitor revenues and expenditures as required by the North Carolina Local Budget and Fiscal Control Act. All records and reporting will be in accordance with Generally Accepted Accounting Principles. The basis of accounting within governmental funds is modified accrual. Under this method of accounting, the county records revenue when measurable and available. Enterprise Funds follow the accrual basis of accounting. Under this method of accounting, the county recognizes revenue when earned and expenditures when incurred.

The County will maintain an accounting system that provides strong internal controls designed to provide reasonable, but not absolute, assurance regarding the safeguarding of assets against loss and the reliability of financial records for preparing financial statements and reports. These reports will be the basis for the budget and the Annual Comprehensive Financial Report (ACFR).

An independent public accounting firm will perform an annual audit. Each year the firm will issue an opinion on the county's annual financial statements, with a management letter detailing areas needing improvement, if required. The county provides full disclosure in all regulatory reports, financial statements and bond representations.

The County maintains an inventory of capital assets. The county maintains reports on inventories and depreciation in accordance with governmental accounting standards.

The ACFR is prepared according to the standards necessary to obtain the Certificate of Achievement for Excellence in Financial Reporting from the Government Finance Officers Association (GFOA). The county submits the ACFR to the GFOA annually with the goal of receiving the designation.

Cash Management Policy

The purpose of the County's Cash Management Policy is to provide guidelines to maximize the use of public funds in the best interest of the public.

Receipts

The county collects cash as quickly as possible to provide secure handling of incoming cash and to move funds into interest earning accounts and investments. Staff deposits funds as required by law and does so in a manner to receive credit for that day's interest. The county maintains cash flow projections to allow investment of funds for longer periods at higher rates of return.

Cash Disbursements

The county seeks to retain money for investment for the longest appropriate period. Staff process disbursements in advance of or on the agreed-upon contractual date of payment, unless earlier payment provides an economic benefit to the County.

The county maintains inventories and supplies at the minimum appropriate level for operations to increase cash availability for investment.

For County checks, dual signatures are required. Facsimile signatures are safely stored and used as appropriate.

Investment Policy

It is the policy of the County to preserve capital and invest public funds to provide the highest investment return with maximum security, while meeting the daily cash flow demands of the County. All county investments conform to all state and local statutes governing the investment of public funds. This investment policy applies to all financial assets in the County's investment portfolio except debt proceeds. The county accounts for and invests debt proceeds separately from other funds. The County's Annual Comprehensive Financial Report (ACFR) accounts for these funds.

Staff use the "prudent person" rule for investments. The "prudent person" concept discourages speculative transactions. It attaches primary significance to the preservation of capital and secondary importance to the generation of income and capital gains. Authorized staff, if acting in accordance with written procedures and state statutes and exercising due diligence, shall be relieved of personal responsibility for an individual security's credit risk or market price changes, provided that these deviations are reported immediately and action is taken to control adverse developments.

The primary investment objectives, in priority order, are safety, liquidity and yield. First, safety of principal is the foremost objective of the investment program. Investments seek to ensure the preservation of capital in the overall portfolio. To attain this objective, diversification is required so potential individual losses cannot exceed income generated from remaining investments. Second, the County's investment portfolio will maintain sufficient liquidity to enable the County to meet all operating requirements by using structured maturities and marketable securities. Finally, the County's investment portfolio will attain a market rate of return.

North Carolina General Statute 159-25(a) 6 delegates management responsibility for the investment program to the Finance Director. The Finance Director will establish and maintain written procedures for the operation of the investment program consistent with this policy. Such procedures will include explicit delegation of authority to persons responsible for investment transactions. No person may engage in an investment transaction except as provided under the terms of this policy and the procedures established by the Finance Director. The Finance Director will be responsible for all transactions undertaken and will establish a system of controls to regulate the activities of subordinates.

Officers and employees involved in the investment process will refrain from personal business activity that could conflict with proper execution of the investment program, or which could impair their ability to make impartial investment decisions. Employees and investment officials will disclose to the County Manager any material financial interests in financial institutions that conduct business within this jurisdiction and they will further disclose any large personal financial/investment positions related to the performance of the County's portfolio. Employees and officers will subordinate their personal investment transactions to those of the County, particularly with regard to the time of purchase and sales.

The Finance Director will maintain a list of financial institutions authorized to provide investment services. The county selects authorized financial institutions based on credit worthiness. Financial institutions must also maintain a physical office in the State of North Carolina. These may include "primary" dealers or regional dealers that qualify under Securities & Exchange Commission Rule 15C3-1 (uniform net capital rule). The county deposits funds to a qualified public depository as required by state law.

All financial institutions and broker/dealers who desire to become qualified bidders for investment transactions must supply the Finance Director with the following: audited financial statements, proof of National Associations of Security Dealers Certifications, proof of state registrations and certification of having read the County's investment policy. Staff will conduct a review of the financial condition and registrations of qualified bidders. The Finance Director may remove from the list financial institutions, brokers and/or dealers that fail to supply requested information.

The County is empowered by North Carolina G.S. 159-30(c) to invest in the following types of securities:

- Obligations of the United States or obligations fully guaranteed as to both principal and interest by the United States.

- Obligations of the Federal Financing Bank, the Federal Farm Credit Bank, the Bank for Cooperatives, the Federal Intermediate Credit Bank, the Federal Land Banks, the Federal Home Loan Banks, the Federal Home Loan Mortgage Corporation, the Federal National Mortgage Association, the Government National Mortgage Association, the Federal Housing Administration, the Farmers Home Administration, the United States Postal Service.

- Obligations of the State of North Carolina Bonds and notes of any North Carolina local government or public authority.

- Fully collateralized certificates of deposit issued by any bank or savings and loan organized under the laws of the State of North Carolina.

- Prime quality commercial paper bearing the highest rating of at least one nationally recognized rating service and not bearing a rating below the highest by any nationally recognized rating service that rates the particular obligation.

- Bankers acceptances of a commercial bank or its holding company provided that the bank or its holding company is either: Incorporated in the State of North Carolina; or Has outstanding publicly held obligations bearing the highest rating of at least one nationally recognized rating service and not bearing a rating below the highest by any nationally recognized rating service that rates the particular obligations.

- Participating shares in a mutual fund for local government investment provided the investments of the fund are limited to those qualifying for investment under this subsection and the Local Government Commission certifies the fund.

- Evidences of ownership of, or fractional undivided interest in, future interest and principal payments on either direct obligations of the United States government or obligations the principal of and the interest on which are guaranteed by the United States, which obligations are held by a bank or trust company organized and existing under the laws of the United States or any state in the capacity of custodian.

- Repurchase agreements with respect to either obligations of the United States or obligations the principle of and the interest on are guaranteed by the United States. This applies if entered into with a broker or dealer, as defined by the Securities Exchange Act of 1934, which is a dealer recognized as a primary dealer by a Federal Reserve Bank, or any commercial bank, trust company or national banking association, the deposits of which are insured by the Federal Deposit Insurance Corporation or any successor thereof.

The county conducts all transactions, including collateral for repurchase agreements, on a delivery-versus-payment basis. A contracted third party custodian designated by the Finance Director holds securities as evidenced by safekeeping receipts.

The County will diversify its investments by institution. With the exception of U.S. Treasury securities and agencies and authorized pools, no more than 35% of the County's total investment portfolio will be invested with a single security type or with a single financial institution.

It is desirable to diversify by security type; however, if the yield is higher, more than 35% of the County's total investment portfolio may be invested in the same security type. To the extent possible, the County will attempt to match its investments with anticipated cash flow requirements. Beyond identified cash flow needs, investments will be purchased so that maturities are staggered to avoid undue concentration of assets in a single maturity range, however, the County will not directly invest in securities maturing more than five (5) years from the date of purchase. The County may collateralize its repurchase agreements using longer-dated investments not to exceed ten (10) years to maturity.

It is the County's full intent, at the time of purchase, to hold all investments until maturity to ensure the return of all invested principal dollars. However, economic or market conditions may change, making it in the County's best interest to sell or trade a security prior to maturity.

All moneys earned and collected from investments other than bond proceed earnings will be allocated quarterly to various fund amounts based on the quarter's average cash balance in each fund as a percentage of the entire pooled portfolio. Earnings on bond proceeds will be directly allocated to the same proceeds.

The Finance Director is responsible for preparing a monthly investment inventory report, which includes investment types, cost, market value, maturity date and yield.

Contract Administration Policy

It is the policy of the County to maintain an efficient and uniform process for the administration of contracts. The contract process aligns with the County's Procurement Policy. It is also the intent of the County to consolidate contracts where appropriate to reduce paper flow and administrative costs.

There are several general rules for contract administration:

- The Department Head, County Manager or Chairman of the Board of Commissioners must sign contracts according to the authority prescribed in the Procurement Policy.

- If a contract is in writing, staff must keep an original in the contract file (in the Contract Administrator's Office).

- The Finance Director (or designee) must pre-audit and encumber all contracts requiring spending. G.S. 159-28 (a) states that if an obligation is evidenced by a contract or agreement requiring payment of money, the contract or agreement shall include on its face a certificate stating that the instrument has been pre-audited. The certificate, which shall be signed by the finance officer or any deputy finance officer approved for this purpose by the governing board, shall take substantially the following form: "This instrument has been pre-audited in the manner required by the Local Government Budget and Fiscal Control Act."

G.S. 159-28 (a) also states that an obligation incurred in violation of this subsection is invalid and may not be enforced and the finance officer shall establish procedures to assure compliance with this subsection.

Although not all contracts obligate the County to make a payment of money, it is nevertheless important to have a system that organizes and catalogs all contracts involving the County. The administrative procedures and guidelines of this policy are not herein included, due to space limitations.

Personnel Management Policy Cabarrus County Commissioners have supported the recruitment and retention of county staff through the following compensation and benefit initiatives:

- Cost of Living Allowance

- Effective at the first full pay period of each fiscal year, a 1% cost of living allowance will be applied to employee salaries.

- Market Comparison of Salaries

- Market compensation and/or classification studies have typically been conducted annually with each department on a two-year review cycle. This year, a "hot jobs" study will be done on positions with high turnover. Studies will be performed by an outside consultant to maintain a pay scale consistent with like jobs in the local market including similar governmental entities. Recommendations will be presented to the Board of Commissioners upon completion of each project and funding will be approved in line with the County budget.

- 401K Plan

- A five percent 401K contribution for non-law enforcement employees will be granted, thus providing them the same benefit as mandated by the State for law enforcement employees.

- Longevity

- The County re-implemented a longevity pay plan in 2023 to recognize employee service to the County. Longevity award is offered one time per year for those employed at the time of payment with a graduated payment tier structure.

- Merit Pay

- The County funds merit pay for employees based on performance (per merit pay scale and performance scores). Current maximum of 4%.

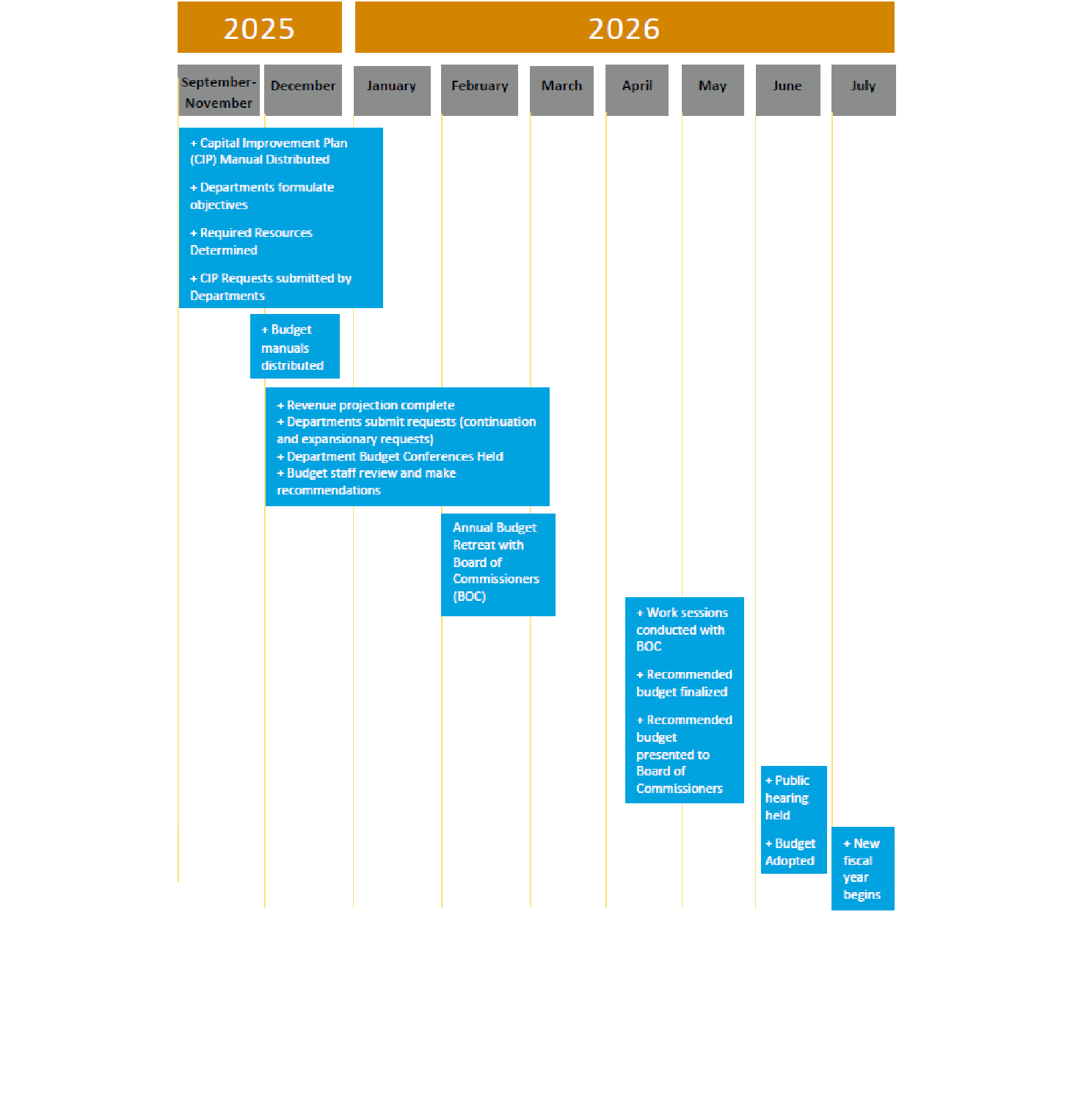

The County's annual budget process seeks to align Board and community priorities with the funding needed to achieve them. The budget process typically occurs during the eight-month period from November to June. The North Carolina Local Government Budget and Fiscal Control Act (G.S. 159, Article 3) requires local governments to adopt an annual budget by June 30, based on the state mandated fiscal year that runs from July 1 to June 30.

Staff start the budget season with a retreat for the Board of Commissioners to discuss community needs for the following year. The retreat also provides an opportunity for department leadership and outside entities to present current needs and concerns. All agencies of the County submit funding requests to the County Manager by the end of February each year. The County Manager uses these requests as the starting point for developing a recommended budget.

Budget staff manage the process using the following levels:

Level 1 - Base

This level starts with the prior year's adopted budget amounts but removes any one-time costs or projects. Departments do not do anything in this level.

Level 2 - Department Continuation

Departments update their budget detail in this level. Prior year detail serves as the starting point, but departments still need to assess and update all prior year detail and amounts while adding new detail if necessary. Continuation budgets provide the same level of service in the coming year that the department is providing in the current year. Such budgets typically include items that repeat year after year. It is ok to have increases in this column due to an increase in the cost of doing business year over year (i.e. inflation costs in operations, supplies, fuel, utilities, contractual increases, etc.). Departments should enter revenues the same as in the past. Departments key in this level.

Level 3 - Manager Continuation Budget Recommendation

This level starts with the Departmental continuation budgets keyed in level 2. Management will review all continuation requests prior to opening up any Departmental expansion budget keying. Management will review requests and make any necessary updates and/or modifications. This review includes analysis of current year and previous years spending. The Budget team will communicate any changes made. Departments do not do anything in this level.

- Level 4 - Department Expansion or Reduction Budget

- This level will only be for new budget requests that the Department is seeking if the capacity for expansion exists.

- The following classify as an expansion request

- new personnel, new software, new technology for new personnel, new projects, new upgrades, new programs, new services, new vehicles for new personnel or adding to the fleet outside of the normal replacement cycle. Expansion requests should be well justified.

- The following revenues are classified as expansion

- those tied to a new grant, new reimbursement due to a new position or a new fee structure. Departments key expansion or reductions in this level.

Level 5 - Manager Expansion or Reduction Budget Recommendation

Budget staff will move to this level prior to departmental budget conferences in March. The goal is to have budget conferences primarily focus on expansion requests that the Department is seeking since Management will review continuation requests ahead of time. Increases or decreases that may take place at the budget conferences will be reflected in this level. Departments do not do anything in this level.

Level 6 - Board

This level will combine Manager recommended continuation and expansion or reduction budget levels (Levels 3 and 5). Budget staff will move to this level after the budget conferences and all adjustments are made in the Manager's level. Budget staff will balance the budget in this level. Any adjustments that take place at the budget workshops in June will be reflected in this level and ultimately the budget will be adopted in this level. Departments do not do anything in this level.

Any changes made after the Board approves the budget go through the Budget Amendment process (see section on Amendments to the Budget Ordinance).

PUBLIC ENGAGEMENT

The public has several opportunities for engagement in the budget process. These opportunities include:

Budget Blueprint -

This is an event that provides the public and opportunity to learn about the process of building the county's budget. It provides a fast, informative look at the inner workings of the county budget. Gov 101 - This is an annual event that provides the public an opportunity to become part of the conversation as the County's budget office breaks down the details and highlights of the upcoming fiscal year spending plan. This course gives the opportunity to meet with department heads, leadership and elected leaders and provide valuable input BEFORE the Board of Commissioners takes public comment and votes on the budget. Budget Work Sessions - These are work sessions on the Budget held by the Board of Commissioners to explore the fiscal year budget being developed in in greater detail. Input at these work sessions are provided by county leadership and staff. These work sessions also provide the Board of Commissioners and the public an opportunity to hear from our community partners. These work sessions are open to the public. Budget Public Hearing - The public hearing provides the opportunity for the public to provide their input on the proposed budget to Board of Commissioners prior to the vote to adopt the budget. Board of Commissioners Meetings - The public also has an opportunity during the regular monthly meetings to provide their input on any topic of concern including the budget.

Budget Adoption

The annual budget serves as the foundation for the County's financial planning and control. Chapter 159 of the North Carolina General Statutes prescribes a uniform system of budget adoption, administration and fiscal control. Not later than July 1, the Board of Commissioners is required to adopt a budget ordinance making appropriations and levying taxes for the budget year in such sums as the Board may consider sufficient and proper, whether greater or less than the sums recommended in the adopted budget. The budget ordinance authorizes all financial transactions of the County except:

Those authorized by a project ordinance; Those accounted for in an intra-governmental service fund for which a financial plan is prepared and approved; and Those accounted for in a trust or agency fund established to account for moneys held by the local government or public authority as an agent or common-law trustee or to account for a retirement, pension, or similar employee benefit system. Those funds listed above that are not budgeted annually are included in the audited financial statements of the County. Therefore, budgets are adopted for the General Fund, Community Investment Fund, Landfill Fund, Arena and Events Center Fund, 911 Emergency Telephone Fund, Social Services Fund, Intergovernmental Fund, Opioid Settlement Fund, Workers Compensation & Property Liability Fund and Self Insurance Health & Dental Fund.

Amendments to the Budget Ordinance

Except as otherwise restricted by law, the Board may amend the budget ordinance at any time after the ordinance's adoption in any manner, so long as the ordinance, as amended, continues to satisfy the statutory requirements. However, except as otherwise provided in this section, no amendment may increase or reduce a property tax levy or in any manner alter a property taxpayer's liability, unless a court of competent jurisdiction or State agency having the power to compel the levy of taxes orders the board to do so. If after July 1, the County receives revenues that are substantially more or less than the amount anticipated, the Board may, before January 1 following adoption of the budget, amend the budget ordinance to reduce or increase the property tax levy to account for the unanticipated increase or reduction in revenues. As allowed by statute, the Board has authorized the County Manager and/or Budget Director, or designee to transfer moneys from one appropriation to another or within the same fund, or modify revenue and expenditure projections, subject to such limitations and procedures as it may prescribe. The budget ordinance includes these limitations and procedures.